You have the script. You have the cast. You have a distribution deal signed in ink. But when you look at your spreadsheet, there is a hole in the middle of your budget that won’t close. This is the moment every producer dreads. The gap between what you promised the bank and what you actually need to shoot the movie is real, and it can kill your project faster than bad weather on set.

This financial void is known as gap financing. It is not a magic fix for a broken business plan. It is a specific tool used to bridge temporary cash flow mismatches during production. If you do not understand how it works, who provides it, and what collateral you must risk, you might find yourself owing money to investors while holding a half-finished film.

The Anatomy of a Film Budget Gap

Film budgets are rarely static. They are living documents that shift based on location costs, actor fees, and unforeseen logistical nightmares. When a producer secures initial funding-often through equity investors or pre-sales-they usually cover about 70% to 80% of the total budget. The remaining amount is the "gap."

Why does this gap exist? Often, banks will only lend against hard assets like intellectual property rights or confirmed pre-sales. They hesitate to fund the risky phase of principal photography. Meanwhile, equity investors may be hesitant to put up more cash until they see proof of concept or completed footage. This leaves a vacuum where the production needs cash to pay crew salaries and rent equipment, but no single source is willing to provide it all at once.

Gap financing steps in here. It is a loan designed specifically to fill this shortfall. Unlike a standard bank loan, which looks at your personal credit score, gap financing looks at the film itself as the asset. The lender bets on the movie’s potential revenue, not just your ability to repay.

How Gap Financing Works in Practice

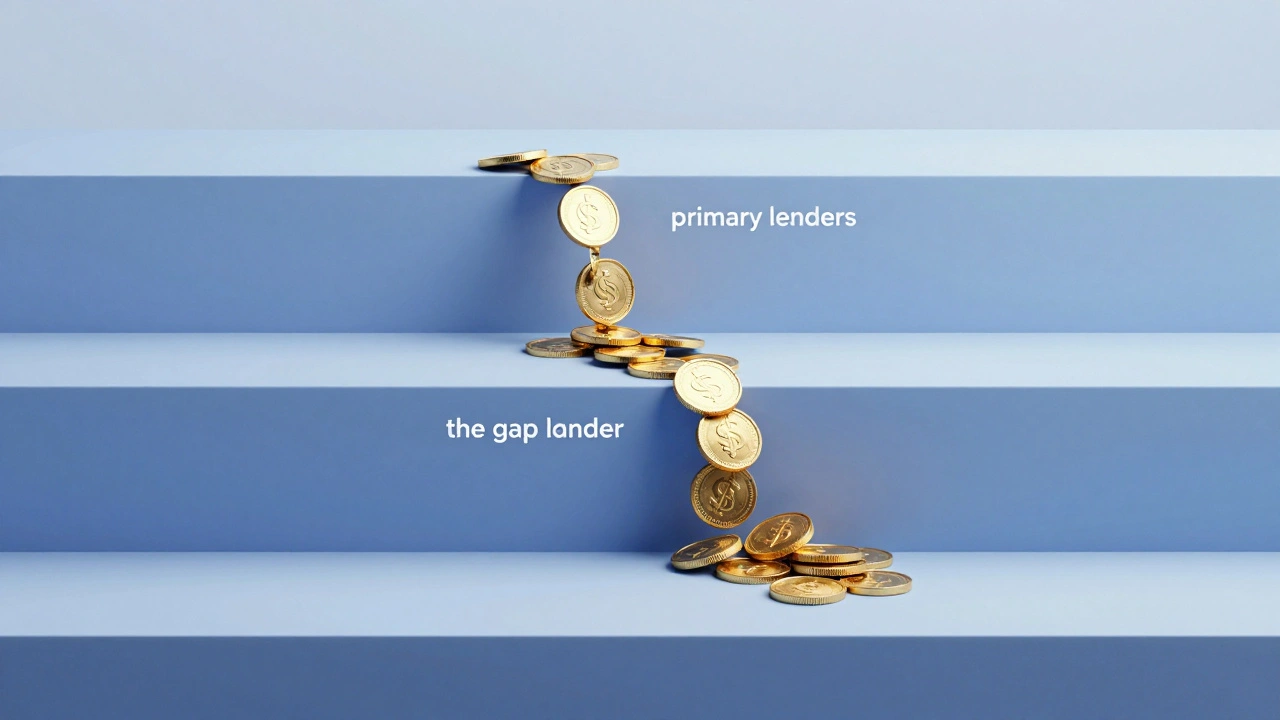

To get gap financing, you typically approach a specialized lender or an existing investor who agrees to provide additional funds. These funds are usually structured as a deferred payment or a second-position loan. This means the gap lender gets paid back after the primary lenders (like banks) have been satisfied from the film’s gross receipts.

Here is the critical part: the gap lender requires security. They will ask for a negative pledge agreement. This legal document prevents you from pledging the same assets to another lender without their permission. It also often includes a clause that gives them control over certain aspects of the production if things go wrong. You are trading some autonomy for cash flow.

In many cases, gap financing is provided by the same entities that hold the first-mortgage debt. For example, a major studio might provide the bulk of the funding, while a smaller independent finance company fills the gap to ensure the production stays on schedule. This keeps everyone aligned because if the movie fails, everyone loses.

Key Players in the Gap Financing Ecosystem

Not every bank offers gap financing. Traditional commercial banks are generally too conservative for the high-risk nature of filmmaking. Instead, you will deal with specialized entities:

- Completion Bond Companies: These firms insure the completion of the film. They often facilitate gap financing because they have a vested interest in ensuring the movie finishes on time and on budget.

- Sales Agents: Sometimes, sales agents who have secured pre-sales can advance funds against future royalties. This is a form of gap financing, though it reduces your long-term profit share.

- Private Equity Funds: Specialized media funds may offer gap loans as part of a broader investment strategy, looking for tax incentives or cultural impact alongside returns.

- Production Insurance Providers: While they don’t lend money directly, their policies are often required by gap lenders to mitigate risk.

Understanding who holds the power in these relationships is crucial. A completion bond company, for instance, has significant leverage. If they perceive the director is going over budget, they can step in and replace key personnel. Gap lenders watch these moves closely.

Risks and Pitfalls to Avoid

Gap financing is not free money. It comes with strings attached that can tighten around your neck if you are not careful. One major risk is the cost of capital. Interest rates on gap loans can be higher than traditional bank loans because of the perceived risk. You must factor this into your bottom line.

Another pitfall is misalignment of interests. If your gap lender is a small private firm, they might push for creative decisions that maximize short-term returns rather than artistic integrity. For example, they might insist on casting a less expensive actor who has better international appeal, even if it hurts the story. Always negotiate clear boundaries in your contracts regarding creative control.

There is also the risk of "cross-collateralization." If you have multiple films in development, a gap lender might require that all your projects serve as collateral for one loan. If one film flops, it could jeopardize the funding for your next project. This is why experienced producers keep their slate diverse and separate.

| Source Type | Cost (Interest/Fees) | Control Level | Speed of Access | Best For |

|---|---|---|---|---|

| Bank Loan | Low-Medium | High | Slow | Established producers with strong collateral |

| Gap Financing (Specialist) | Medium-High | Medium | Fast | Bridging immediate production shortfalls |

| Equity Investors | None (but dilutes ownership) | Variable | Very Slow | Long-term partnerships and creative freedom |

| Crowdfunding | Platform Fees | Low | Medium | Audience building and niche markets |

Navigating Legal and Financial Structures

The legal framework surrounding gap financing is complex. You will need lawyers who specialize in entertainment finance. They will draft the intercreditor agreement, which defines the relationship between different lenders. This document ensures that if the film earns money, everyone knows exactly when and how much they get paid.

Pay attention to the "waterfall" structure. This is the order in which revenues are distributed. Typically, it goes: theatrical distributors take their cut, then direct expenses are reimbursed, then first-priority lenders get paid, and finally, gap lenders receive their share. Only after all debts are settled do equity holders see profit. Understanding this sequence helps you manage expectations with your partners.

Tax incentives also play a role. In regions like Georgia, UK, or Canada, government rebates can effectively reduce the gap you need to finance. Smart producers structure their deals so that these rebates are assigned directly to the gap lender, reducing the amount of cash needed upfront. This makes the loan safer for the lender and cheaper for you.

Alternatives to Traditional Gap Financing

If gap financing feels too risky or expensive, there are alternatives. One option is deferred compensation. Key crew members or actors agree to be paid later, out of the film’s profits. This reduces the immediate cash requirement but can strain relationships if the film underperforms.

Another alternative is crowdfunding. Platforms like Kickstarter allow you to raise small amounts from many people. While this doesn’t solve large budget gaps, it can cover marketing costs or specific production elements, freeing up other funds. However, crowdfunding requires significant time and effort to manage community expectations.

Some producers turn to tax equity partnerships. These are common in larger productions where tax credits can be monetized. Institutional investors buy the tax credits in exchange for a portion of the production’s income. This is a sophisticated tool that requires professional guidance but can significantly lower the net cost of production.

Real-World Scenarios: When Gap Financing Saves the Day

Consider a mid-budget thriller shooting in New York City. The producer has secured $5 million from equity investors and a $2 million pre-sale to a streaming platform. The total budget is $8 million. There is a $1 million gap. The production faces unexpected overtime costs due to weather delays. Without gap financing, the crew would walk off the job.

In this scenario, a specialist lender provides a $1 million gap loan secured by the film’s underlying rights. The lender receives a 10% return on the loan plus a small percentage of net profits. The production continues, the film is completed, and upon release, the gap loan is repaid from the first box office receipts. Everyone wins, provided the film performs adequately.

Conversely, imagine a low-budget indie drama. The gap is only $50,000. Seeking formal gap financing might be overkill due to legal fees. Here, a personal loan from a trusted associate or a small grant from a local arts council might be more efficient. Not every gap requires a complex financial instrument.

Strategic Planning for Future Productions

Experienced producers plan for gaps from day one. They build contingency funds into their initial budget, usually 10% to 15%. This buffer reduces the size of the gap they need to finance later. It also shows lenders that you are prudent and realistic about risks.

Building relationships with gap lenders before you need them is essential. Attend industry events, network with finance executives, and establish trust. When you have a hot script and a tight deadline, you want a lender who already knows your track record. Cold calls rarely result in favorable terms.

Finally, maintain transparency. Hide nothing from your financiers. If costs rise, communicate early. Lenders respect honesty and proactive problem-solving. They fear surprises more than bad news. By keeping everyone informed, you create a collaborative environment where solutions can be found quickly.

What is the difference between gap financing and bridge financing?

While similar, bridge financing is typically used to cover short-term cash needs until permanent financing is secured, often in real estate. Gap financing in film is specifically tied to the production budget shortfall and is secured against the film's assets and future revenues. Bridge loans are usually interim; gap loans are integral to the production cycle.

Who qualifies for gap financing?

Producers with a solid track record, a viable script, attached talent, and a partial budget covered by other sources qualify. Lenders look for mitigated risk, such as completion bonds, pre-sales, or tax incentives. First-time producers may struggle unless they have strong backing from established entities.

How much does gap financing cost?

Costs vary widely. Interest rates can range from 8% to 15% or higher, depending on the risk profile. Additionally, lenders may charge origination fees, commitment fees, and a percentage of net profits. Always calculate the total cost of capital, not just the interest rate.

Can I use gap financing for post-production?

Yes, but it is less common. Most gap financing is focused on principal photography. Post-production gaps are often covered by deferred payments from editors or visual effects houses. However, if the overall budget is underfunded, a gap loan can cover all phases.

What happens if the film fails to recoup the gap loan?

The lender can seize the collateral, which usually includes the film’s rights and any remaining assets. They may also pursue legal action against guarantors. This is why understanding the security package and limiting personal guarantees is crucial for producers.

Comments(5)